Go global: how AI is reshaping fixed income markets

Why we believe using a global lens matters when capturing potential AI opportunities within fixed income markets.

This is the second article in a three-part series that discusses how recent advances in AI make the case for taking an active, global, and unconstrained approach to fixed income investing. Here we explore why we believe a global approach can help investors navigate the fast-evolving AI story.

Read the first article here.

The surge in AI-related capital expenditure is reshaping global fixed income markets. This is not only through record bond issuance volumes but also through how and where that issuance is being bought.

For investors, the opportunity is no longer simply to participate in attractive new supply, but to identify curve- and tranche-level dislocations that arise because different investor bases demand different bonds, with differing maturity levels, currencies or features.

We believe a global approach can take advantage of these structural differences through relative value positioning, while also helping to mitigate broader risks through credit diversification. Alphabet’s* multicurrency bond issuance in February, including its landmark 100-year sterling bond, provides a clear case study.

So why sterling and why 100 years?

Alphabet’s decision to issue a century bond and do so in sterling rather than dollars was intentional, not random. The sterling market has a well‑established buyer base of UK pension funds and insurers with long-dated liabilities, for whom ultra‑long duration is not a risk but a necessity.

In addition, as the first big technology issuer with a AA-range rating in the sterling market, demand for this issue was naturally higher due to the potential diversification benefits.1 Order books were many times oversubscribed, despite the maturity being highly unusual for a technology issuer.

A divergence in markets

This highlights a crucial point for global fixed income investors: bonds issued by the same borrower can trade very differently depending on who the marginal buyer is and other market technicals at play.

In sterling, liability-driven investors often prioritise duration and cashflow matching over spread, compressing yields at the ultralong end of the curve. In contrast, the same issuer’s long-dated USD bonds are more likely to be owned by total return managers and insurance portfolios with stricter spread discipline.

This divergence can create persistent valuation gaps across yield curves and currencies. When one segment of the curve clears easily and another requires additional concession, kinks and dislocations emerge, both within a single market and across markets.

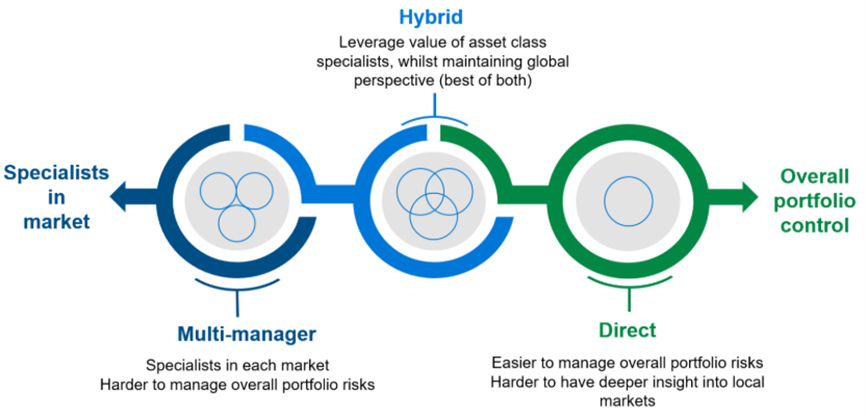

So how does a global approach, which leverages regional asset class specialists, help capitalise on these opportunities?

[1] It should be noted that diversification is no guarantee against a loss in a declining market

Looking through a global lens

Many regional bond markets are dominated by investors focused solely on that particular market (e.g. sterling bond market). A global approach allows us to take advantage of cross-currency opportunities where the same issuer issues in multiple bond markets. A global framework simply expands the opportunity set from ‘which bond to own’ to “in which market is it best to own this issuer’. Domestic focused investors would not necessarily be looking as closely at these opportunities.

With AI hyperscalers starting to turn to other markets outside of the USD market, relative value opportunities within the sector are growing. By employing a hybrid approach we are able to leverage the value of asset class and regional specialists in uncovering specific market technicals, while maintaining a global perspective to seek to identify and capitalise on them.

A truly diversified approach is key

A key risk we are currently monitoring is market sentiment towards issuance outside of the dollar market. Hyperscaler capital expenditure (capex) plans – widely forecast to exceed $500 billion in 20262 –are catalysing fears about record investment grade supply across currencies. While Alphabet’s sterling deal was well received, the size and liquidity of the sterling market mean the likelihood of indigestion may come sooner than expected if other hyperscalers follow suit.

With this in mind, we continue to believe that a global approach which broadens diversification is important at a time when AI disruption is concentrated in developed markets. Research from the International Monetary Fund3 and others shows that AI exposure and preparedness are materially higher in advanced economies, implying that much of the AI‑related capex—and associated credit supply—will be borne by developed‑market issuers. Emerging markets, by contrast, face less immediate disruption and issuance pressure in our view, providing an additional dimension of relative value and risk balance in global portfolios.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

[2] L&G as at 1 April 2026

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

[3] International Monetary Fund, April 2025

Key risks

The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested.

Whilst L&G has integrated Environmental, Social, and Governance (ESG) considerations into its investment decision-making and stewardship practices, this does not guarantee the achievement of responsible investing goals within funds that do not include specific ESG goals within their objectives.

The risks associated with each fund or investment strategy should be read and understood before making any investment decisions. Further information on the risks of investing in this fund is available in the prospectus here: