Implications of reducing the carbon footprint of factor strategies

In a new research paper, we provide a detailed analysis of how factor strategies’ carbon footprint can be reduced and its implications.

The below is a summary of our new whitepaper: Implications of reducing the carbon footprint of equity factor portfolios.

Factor-based equity strategies have more than $1.5 trillion1 in assets under management, reflecting investors’ rising appetite for this innovative approach to indexation.

Simultaneously, demand for reducing the carbon footprint of investment strategies (decarbonisation) has increased as investors seek to align their portfolios with net zero objectives.

These two trends raise an important question: can factor strategies be decarbonised?

The starting point

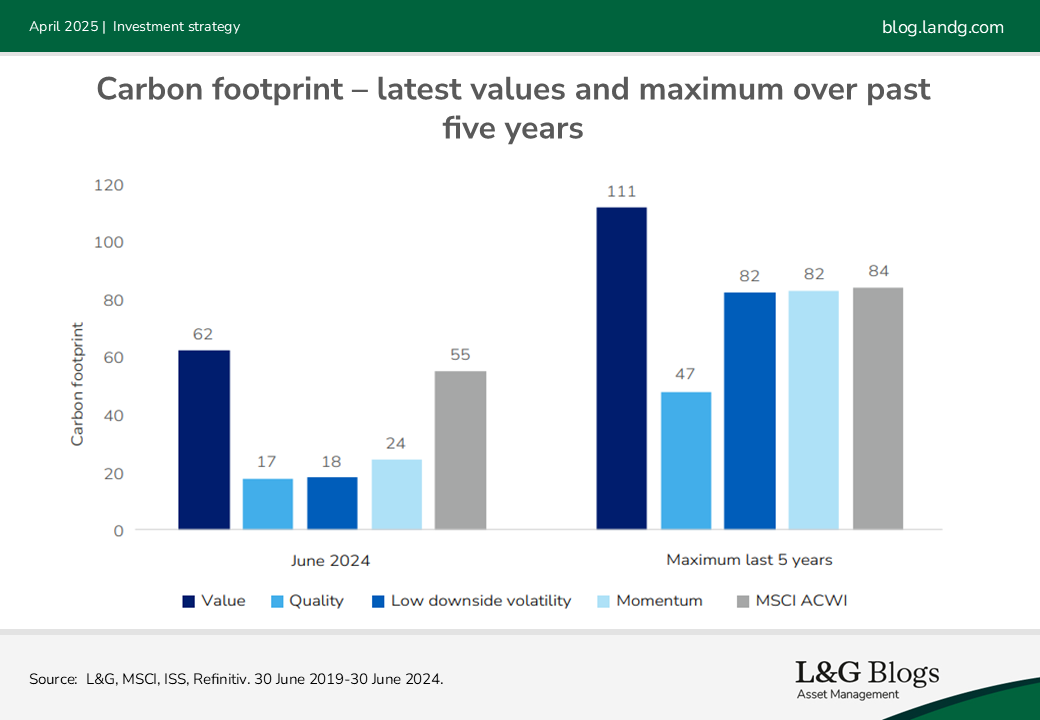

Before assessing how factor strategies can be decarbonised, we analysed the typical carbon footprint of the most popular equity factors.

Using a global benchmark representing developed and emerging markets and our factor scoring signals, we constructed top-tercile equity portfolios2 for four popular factors. This allowed us to compare their carbon footprint with a market-cap index over 10 years. We present below the current carbon footprint and the maximum over the past five years.

It’s apparent that different factors have different carbon footprints – and that with one clear exception, factor strategies may compare favourably with a market-cap strategy.

The value factor tends to be the most carbon intensive, while the quality factor tends to be least carbon intensive. Price-driven factors such as low volatility and momentum, meanwhile, exhibit wider carbon footprint ranges.

The role of sector exposures

It’s well known that three sectors contribute the majority of (weighted) emissions – Materials, Utilities and Energy, with Industrials following to a lesser extent.

This turns out to be highly relevant when considering the decarbonisation of factor strategies.

Strategies that are overweight high-carbon sectors may be more challenging to decarbonise effectively without affecting factor style exposure.

For top-tercile factor portfolios:

- Value tends to have a significant overweight to Financials and Energy, and a significant underweight to Information Technology.

- Quality tends to have a significant overweight to Information Technology.

- Low downside volatility tends to be overweight defensive sectors such as Consumer Staples and Healthcare.

- Price-driven factors (low downside volatility and momentum) can display larger dispersion of sector allocations over time.

It can be done – but the details matter

Having established the starting point, we then assessed the merits of two methods of decarbonising factor strategies: exclusions and tilting. We considered how effectively carbon exposure could be reduced, how factor potency was affected, and the effect on risk and return profiles.

Overall, our headline findings were promising: factor strategies can indeed be meaningfully decarbonised without fundamentally affecting their utility for investors and sacrificing factor exposures.

However, there are several fascinating nuances. Read our research paper to discover our findings on the following:

- What are the pros and cons of exclusions and tilting, and are there particular sectors that may be affected differently by the two methods?

- How do decarbonised factor strategies fare in regional rather than global markets – particular those markets that have significant sector biases?

- Which types of portfolios could potentially suffer a ‘tug of war’ between strong factor scores and weak carbon metrics? How can this be overcome?

Read the research here: Implications of reducing the carbon footprint of equity factor portfolios.

1. Source: Bloomberg, L.P., data through 12/31/2023.

2. Top tercile equity factor portfolios are groups of stocks chosen because of their high ranking on specific characteristics that define those factors.