Time to shine for EM debt

Investors can no longer overlook the performance and influence of emerging markets (EM) in the global economy. After delivering robust returns in 2025 despite global volatility, selective parts of the EM debt universe deserve a bigger role in global allocations, say L&G’s Ben Bennett, head of investment strategy for Asia, and Uday Patnaik, head of Asia fixed income and global EM debt.

EM fundamentals now speak for themselves. Their strength reflects the increasingly significant role of these economies in international markets – forecast to grow to about 50% of global GDP in US dollar (USD) terms, and 60% in terms of Purchasing Power Parity.1

This influence is to be expected given supportive macro dynamics. External sector and public finances are improving, with trade balances and FX reserves both on positive trajectories. In turn, the latest IMF forecast suggests EM and developing economies will continue to be global growth drivers, with expectations they will expand by 4.2% in 2025 and 4.0% in 2026.2

They are also enjoying positive credit ratings momentum as upgrades outpace downgrades. As a result, EM hard currency sovereigns had returned 10.6% year-to-date as of mid-September, while corporates had gained 7.2%.3

Movements in US Treasuries helped to drive these gains, supported by modest spread tightening – especially in the high yield (HY) segment. EM local markets have outperformed, too, buoyed by a weaker USD.

EM perceptions a myth

On the evidence of the data, we believe many emerging economies can no longer be viewed as second-best to some of the so-called developed market (DM) nations.

Indeed, with sound policies being implemented across various EM countries, they look increasingly like DM.

Broadly, for example, inflation is stable across many EM economies, with debt-to-GDP ratios typically below levels in the G7.4 EM central banks have generally handled inflation better than their DM counterparts by recognising it early and not implementing zero or negative rates.

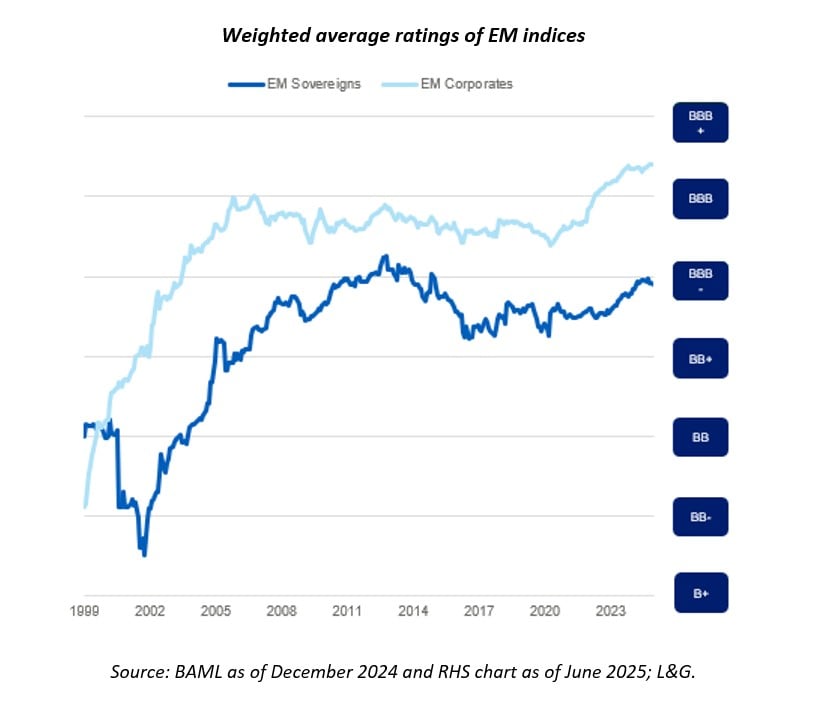

Further, as EM credit ratings have improved over the past two decades, the JP Morgan EMBI Global Diversified Index (sovereign hard currency index) is at around IG rated, while the JP Morgan CMBI BD Index (corporate hard currency Index) is now solidly IG rated.

With all this in mind, we believe now is the time for global investors to reassess their allocation to EM debt.

In particular, EM debt offers a mix of volatility profiles, default rates and drawdown profiles across sovereign IG, sovereign HY, corporate IG and corporate HY.

Capturing EM momentum

Yet despite meaningful inflows into EM debt in 2025 and strong local-currency returns as USD pressure eased and yields in many EMs rallied, credit fundamentals remain mixed. Investors cannot ignore the fact that dispersion across EM countries and sectors is high.

More specifically, there is varying health in sovereign and corporate balance sheets, plus some issuers facing refinancing pressures while others benefit from stronger commodity prices and fiscal buffers. This means credit selection matters, with curve positioning and FX overlay potentially adding value versus passive index exposure.

In their search for value, therefore, investors can choose different parts of the EM universe based on their risk appetite and return requirements.

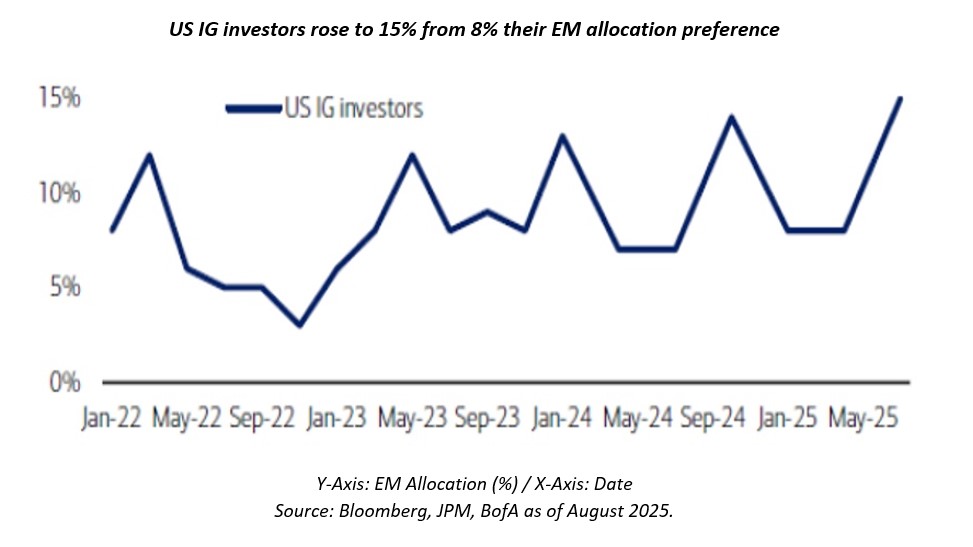

For example, we have seen since early 2025 that US IG investors have increased their EM allocation preference to 15%, up from 8%.

As EM typically performs well during rate-cutting cycles by the US Federal Reserve and when the USD weakens, these portfolios with increased EM allocations might stand to gain from the current macro backdrop.

Further, when considering potential returns for EM sovereign and corporate indices under different scenarios for rates and spreads, should nothing change much with sovereign EM spreads over the course of a year, investors would make about 6.5% on the sovereign index and 5.9% on the corporate index. Should rates rally but spreads remain unchanged, returns could reach about 8% for sovereigns based on yields falling 50 basis points, and about 8% for corporates based on yields falling 75 basis points.5

We believe the investment opportunities in hard currency EM debt is attractive. While local currency could perform well with USD depreciation, many EM countries have already implemented rate cuts, limiting potential gains.

We believe the investment opportunities in hard currency EM debt is attractive. While local currency could perform well with USD depreciation, many EM countries have already implemented rate cuts, limiting potential gains.

Differentiating EM debt

With an outlook that seems constructive but heterogeneous for 2026, EM debt may benefit in the case of a softer USD and where there is scope for EM rate cuts to support local-currency returns and selective hard-currency opportunities.

However, managing idiosyncratic sovereign and corporate risks, as well as geopolitical and trade shocks, must be front of mind for global investors.

This requires active, high-conviction, diversified positioning with disciplined hedging and country selection as a prudent way to capture upside while controlling tail risk. This approach can help to achieve the goal of a total return-orientated approach with an asymmetric return profile – in short, higher and larger positive returns and lower and fewer drawdowns.

Click here for more information on Active Fixed Income at L&G

1 There is no guarantee that any forecasts made will come to pass.

2 Source: IMF, "World Economic Outlook", October 2025 - https://www.imf.org/en/publications/weo/issues/2025/10/14/world-economic-outlook-october-2025

3 Source: L&G, “Active Fixed Income Outlook”, Q4 2025: https://am.landg.com/asset/4a91b3/globalassets/lgim/_document-library/insights/afi_outlook_q4_2025.pdf/

4 Source: Visual Capitalist, “Mapped: Government Debt to GDP by Country in 2025”, October 27, 2025: https://www.visualcapitalist.com/mapped-government-debt-to-gdp-by-country-in-2025/

5 Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

About L&G

Established in 1836, L&G is one of the UK's leading financial services groups and a major global investor, with US$1.533 trillion in total assets under management of which 43% (US$654 billion) is international (Source: L&G, global AUM as at 30 June 2025. Excludes assets managed by associates (Pemberton, NTR, BTR). The AUM includes the value of securities and derivatives positions and may not total due to rounding). L&G's Asset Management business is a major global investor across public and private markets. Our clients include individual savers, pension scheme members and global institutions, who invest alongside L&G’s own balance sheet. Our ambition is to be a leading global investor, innovating to solve complex challenges for our clients using the power of L&G. This is rooted in our investment philosophy and processes, which are focused on creating value over the long term.

Click here for more information

Key risks

The value of investments and the income from them can go down as well as up and you may not get back the amount invested. Past performance is not a guide to future performance. The details contained here are for information purposes only and do not constitute investment advice or a recommendation or offer to buy or sell any security. The information above is provided on a general basis and does not take into account any individual investor’s circumstances. Any views expressed are those of L&G as at the date of publication. Not for distribution to any person resident in any jurisdiction where such distribution would be contrary to local law or regulation.

Issued by:

Hong Kong: Legal & General Investment Management Asia Limited, a Licensed Corporation (CE Number: BBB488) regulated by the Hong Kong Securities and Futures Commission (“SFC”). This material has not been reviewed by the SFC.

Singapore: LGIM Singapore Pte. Ltd (Company Registration No. 202231876W), regulated by the Monetary Authority of Singapore (“MAS”). This material has not been reviewed by the MAS.