Doing things differently: Unconstrained investing in the age of AI

We explore why we believe unconstrained strategies can take a differentiated approach to identify potential AI investment opportunities.

This is the final article in a three-part series that discusses how recent advances in artificial intelligence (AI) make the case for taking an active, global, and unconstrained approach to fixed income investing. Here we explore why we believe unconstrained strategies can take a differentiated approach to identify potential AI investment opportunities. Read the first and second articles.

A substantial proportion of today’s global fixed income market is shaped by investors who follow strict, rule-based frameworks. This includes some passive investors who replicate index performance without deviation, certain pension funds whose primary focus is liability matching rather than yield or spread considerations, and benchmark-aware investors who, despite adopting active strategies, may still be restricted by their funds’ mandates and guidelines.

However, an ‘unconstrained’ approach can allow investors to act differently. Rather than anchoring portfolios to an index, we use an asset allocation approach which focuses on relative value across issuers, geographies, currencies and capital structures. We believe an unconstrained strategy can capture potential opportunities and help mitigate risks across the diverse fixed income spectrum.

Global diversification and flexibility are central to this philosophy, enabling us to respond dynamically to changing market environments.

A reshaping of credit markets

The surge in AI‑related capital expenditure provides a powerful example of why this flexibility matters.

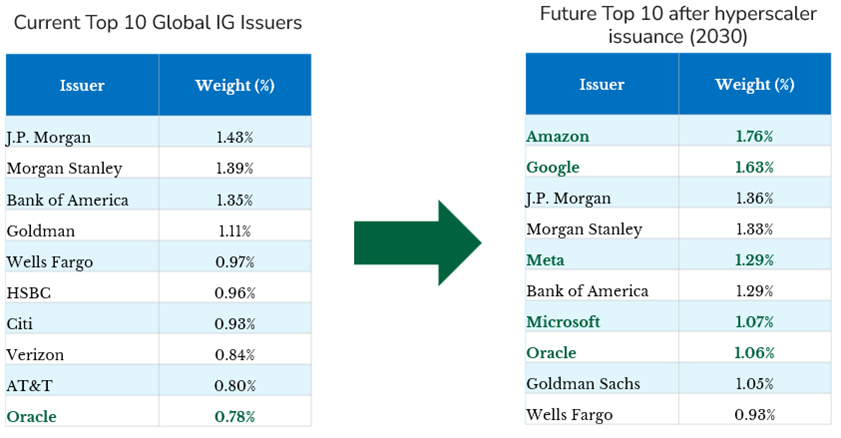

Hyperscalers are committing unprecedented sums to data centres, power infrastructure and chips, increasingly funding this investment through public bond markets. Even those with the strongest balance sheets are now issuing at scale, fundamentally reshaping investment‑grade credit markets.

For example, Alphabet’s* rare 100-year sterling bond issue[1] means that the issuer will now account for 1-3% of key UK investment grade (IG) benchmarks.

If only 25% of the expected AI-related capital expenditure is issued in IG public credit markets, the combined weighting of the five major hyperscalers (Alphabet, Apple*, Amazon*, Microsoft* and Meta*) in the global IG index would increase from 2% to around 7% by 2030[2]. More widely, technology stocks could account for over 20% of the US IG market by this time[3], which we believe poses a significant increase in concentration risk, albeit not at equity levels.

1 Source: Bloomberg, as at 10 February 2026.

2 Source: L&G, Bloomberg, as at March 2026.

3 Source: L&G, Bloomberg, as at March 2026.

Source: L&G, Bloomberg, as at March 2026. For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

What challenges does this present?

So far, the hyperscaler supply has been absorbed without any notable problems, and at least partly for good reason. Alphabet and Meta both paid a clear ‘new issue premium’ of 10 to 15 basis points to access the debt market, compared to previous issues.

Nonetheless, a growing share of this demand for hyperscaler issuance will likely be for necessity rather than preference. When new bonds are incorporated into market indices, investors who track these benchmarks or must manage tracking error constraints are incentivised to acquire them – frequently during month-end rebalancing periods – regardless of their valuation.

Institutional bond investors, such as pension funds, insurers, and mutual funds, typically impose restrictions on sector or issuer exposures to maintain portfolio diversification. However, mandate concentration restrictions typically focus on individual issuers and sectors rather than broader themes and, therefore, may not provide meaning insulation against a widespread decline in AI sentiment.

Consequently, the index may be disproportionately weighted towards companies with future earnings tied to AI themes, potentially creating latent risks that may not be immediately apparent.

Doing things differently: The unconstrained approach

L&G’s unconstrained approach allows us to respond very differently to these dynamics.

We believe an unconstrained approach, coupled with thematic analysis by our Global Research & Engagement Groups (GREGs), may best be placed to manage concentration risks that become too reductionist when considered only through a sectoral or issuer lens.

Rather than automatically absorbing new supply, we can be selective: participating where we believe compensation is attractive and stepping aside where valuations become stretched, all while maintaining diversification.

While hyperscalers have offered new-issue concessions to attract investors, an interesting dynamic we have witnessed is the impact on existing hyperscaler bonds and credit markets in general.

If high-quality AI issuers continue offering attractive yields, it could reset valuations across the corporate bond market, prompting investors to sell lower-quality credits to make room for new tech bonds.

As unconstrained investors, we are not compelled to engage in primary market issuance. We recognise opportunities to trade strategically around issuance trends, both among hyperscaler issuers and by reallocating capital into overlooked areas of the market that are temporarily crowded out by headline issuance.

In summary, we believe a flexible, unconstrained approach is paramount as credit markets are reshaped by the AI theme, which will no doubt create winners and losers. In our view, robust unconstrained strategies can distinguish between these two to selectively own stronger credits and may have an advantage over constrained investors with less freedom to avoid crowded trades.

* For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

Key risks

The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested.

Whilst L&G has integrated Environmental, Social, and Governance (ESG) considerations into its investment decision-making and stewardship practices, this does not guarantee the achievement of responsible investing goals within funds that do not include specific ESG goals within their objectives.

The risks associated with each fund or investment strategy should be read and understood before making any investment decisions. Further information on the risks of investing in this fund is available in the prospectus here: