In a more volatile, inflation-sensitive environment with heightened geopolitical risk, investors can no longer rely on traditional fixed income playbooks.

We believe bonds still matter, credit still offers income and diversification is still key*. But each of these now needs to be approached with greater flexibility and fewer assumptions amid profound shifts in capital flows and uncertainty around growth, rates and policy.

These were some of the key messages from a recent discussion we had in Singapore with a group of institutional investment leaders.

The main takeaway? Portfolio construction is evolving – not away from traditional building blocks, but towards a more balanced combination of benchmark-aware stability and portfolio flexibility.

The evolving role of duration as a hedge

Central to the discussion is the view that the role of duration has changed.

For years, long-duration government bonds acted as a reliable hedge. When equities or credit sold off, yields tended to fall, helping to mitigate downside. That relationship is far less dependable now.

In a world where inflation has trumped recession as the dominant fear, bonds and risk assets can fall together. That creates positive correlation and challenges traditional portfolio construction, particularly the 60/40 model.

The shift is therefore less about replacing one with the other, and more about recognising that duration is no longer a static hedge; it is a variable risk factor that can be managed differently across portfolio layers.

Blending stability and flexibility in portfolios

A typical foundation for portfolios remains benchmark-aware fixed income exposure, providing investment grade (IG) sovereign, credit and securitised exposure across developed markets. That approach aims to offer a highly liquid and transparent ballast in multi-asset portfolios and can act as a diversifier though increasingly regime-dependent correlation versus equities.

We believe such benefits can support the significant volume of fixed income assets already tracking global aggregate benchmarks. And, importantly, despite changing correlations, many investors still value this exposure as a reference point for pricing risk and maintaining portfolio discipline.

However, in our view a scalable and passive core fixed income allocation alone may not be sufficient in today’s regime.

This also reflects sentiment we have increasingly seen in CIOs’ planned allocation changes in 2025 and so far in 2026.

CIOs’ Planned Allocation Changes (%) in Fixed Income, 2026 vs 2025

| Fixed Income Strategy | 2026 | 2025 |

| Active Unconstrained | +12% | +12% |

| Active EM Debt | +11% | +4% |

| Active Core | +7% | +21% |

| Active High Yield | +5% | -3% |

| Passive Fixed Income | -14% | -3% |

Source: 2026 CIO Sentiment Survey from Top1000funds and Casey Quirk. Asset allocation is subject to change.

Global aggregate indices embed structural exposures, particularly to duration and developed market rates, that may not always align with prevailing macro risks. As a result, investors are increasingly pairing core allocations with or “multiverse” strategies.

These flexible mandates can allow managers to achieve several objectives in response to changing conditions: adjust duration meaningfully; allocate across IG, high yield (HY) and emerging market (EM) debt; shift between regions, currencies and sectors; and hold cash or defensive positioning when needed.

In a more unstable correlation regime, investors say they want managers who can preserve capital, not just deliver index-like exposure.

Yet with greater flexibility comes greater scrutiny. In our discussion, several asset owners noted that while they are more willing to allocate to unconstrained strategies, this comes with clear expectations around risk control and drawdown management.

The lesson from recent market stress episodes is clear: flexibility must translate into tangible downside risk mitigation, not just theoretical freedom.

Given the reliable, liquid and transparent anchor benchmark strategies continue to provide, rather than viewing these approaches as substitutes, many investors now see them as complementary:

- Benchmark strategies can provide stability, liquidity and broad market exposure.

- Unconstrained strategies can provide adaptability, drawdown management and alpha potential.

The balance between the two depends on investor objectives, but both can play an important role in modern fixed income portfolios.

Forecasting is futile, understanding consensus counts

Making it even harder to prepare portfolios is the scepticism about macro forecasting.

Trying to predict inflation, growth, central bank decisions or geopolitical outcomes with precision is fraught with difficulty. Instead, focusing on common market behaviour, such as what most investors believe and why, and what might force them to change their minds, can help investors spot and defend against overconfidence, crowded narratives and pricing distortions.

This perspective is especially relevant in today’s environment of strong but fragile convictions.

Opportunities are less about making bold directional calls, and more about identifying where consensus has become crowded or complacent, and positioning portfolios accordingly.

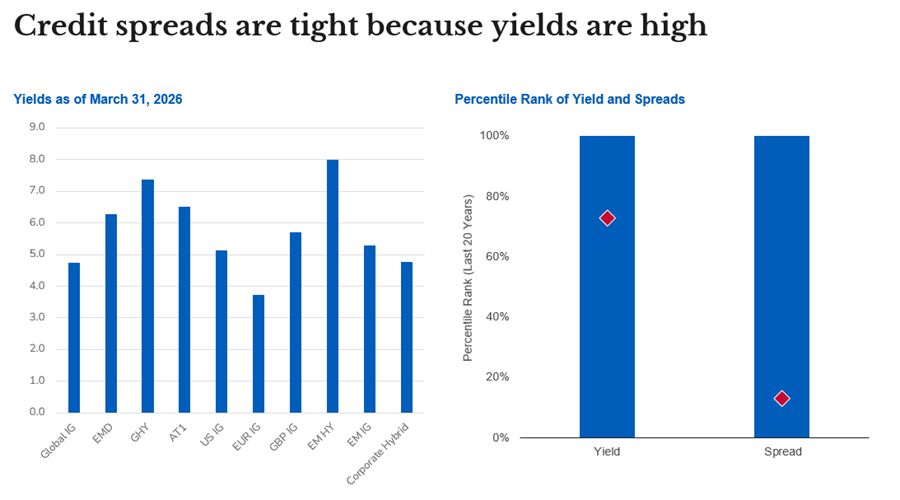

Credit: attractive yields, but spreads offer limited cushion

Looking at exposure to credit, while yields remain attractive, the discussion highlighted that uncomfortably tight spreads create a difficult trade-off.

Fixed income is once again providing income that investors find appealing, and recent increases in yields have supported demand. However, tight spreads mean investors are not being paid much for additional risk, particularly lower-quality or structurally vulnerable exposure.

Source: L&G, Bloomberg, as at 31 March 2026. Data is monthly yield-to-worst and OAS spread for US corporate credit over the 20 years. The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested.

Put simply, investors may like the carry, but they should be much more cautious about the valuation.

This reinforces the importance of selectivity and active decision-making. Credit can still play an important role in portfolios, but manager discretion matters.

For example, benchmark strategies provide broad exposure to IG credit, while more flexible strategies can be more selective, rotating across sectors and quality.

Geopolitics, inflation and diversification

A world of greater fragmentation, supply chain disruption and fiscal activism increases the likelihood of persistent inflation volatility and episodic shocks.

For investors, this increases the need for diversification, but in a broader sense.

It goes beyond owning a mix of stocks and bonds, and towards diversifying across regions, currencies, sectors and investment styles, including both benchmark and unconstrained approaches.

That helps explain increasing interest globally in incremental moves away from concentrated US dollar exposure. Yet, lack of a true alternative means US Treasuries and the dollar remain central to global portfolios for now.

New portfolio ideas and approaches

Several practical ideas emerged from the discussion:

(1) Benchmark allocations remain essential as liquid, scalable core exposures, but should be complemented with active overlays where appropriate.

(2) Duration should be managed actively, whether against a benchmark or for unconstrained fixed income.

(3) Despite high-income fixed income sub-asset classes like HY, EM debt and subordinated debt still potentially offering attractive yields, credit exposure should be selective, given tight spreads and asymmetric risks.

(4) Flexible mandates that can move across IG, HY, securitised assets, EM debt and cash look increasingly valuable, especially to navigate regime shifts and manage drawdowns.

(5) Highly liquid, global active fixed income remain a mainstay in investors’ portfolios, with portfolios becoming more multi-layered.

A more balanced fixed income toolkit

Across the board, the message was clear: investors need more flexibility, more diversification and more humility about forecasting.

Equally, they need robust core exposures that aim to provide stability, liquidity and consistency.

The result is a more balanced approach to fixed income:

- Not abandoning benchmarks but using them more consciously.

- Not relying solely on flexibility but deploying it where it adds value.

Ultimately, that may mean more styles of managers, more geographic breadth and more active risk budgets. As a result, investors are more open to giving managers with a differentiated approach more room to manage risk actively.

In today’s demanding environment, volatility can create more alpha opportunities for investors who are disciplined in their core allocations and deliberate in how they deploy flexibility though being nimble, valuation-aware and willing to challenge consensus.

* The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested. It should be noted that diversification is no guarantee against a loss in a declining market. Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Key risks

The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested.

Whilst L&G has integrated Environmental, Social, and Governance (ESG) considerations into its investment decision-making and stewardship practices, this does not guarantee the achievement of responsible investing goals within funds that do not include specific ESG goals within their objectives.

The risks associated with each fund or investment strategy should be read and understood before making any investment decisions. Further information on the risks of investing in this fund is available in the prospectus here: